Pennsylvania is home to over 1.1 million small businesses, employing nearly half of the state's entire workforce.

From contractors in Pittsburgh to consultants in Philadelphia, every one of those businesses faces real financial risk every single day, and small business insurance in Pennsylvania is what stands between an unexpected event and a potentially devastating loss.

Whether you're launching your first venture or running an established company, the right coverage keeps your business legally protected, financially stable, and positioned to grow no matter what comes your way.

What is Small Business Insurance in Pennsylvania?

Small business insurance in Pennsylvania is a customized package of policies designed to protect your company from the financial consequences of lawsuits, property damage, workplace injuries, and other unforeseen events. No two businesses carry the same risk profile, which is why coverage is built around your specific industry, size, and day-to-day operations, not a one-size-fits-all template.

Types of Small Business Insurance You Need in Pennsylvania

Here are the most essential types of business insurance in Pennsylvania that every small business owner should understand:

General Liability Insurance for Pennsylvania Small Businesses

Who it's for: Any business that interacts with customers, clients, vendors, or the general public.

General liability insurance protects your business if a third party suffers bodily injury or property damage because of your operations. It covers legal defense costs, medical bills, and settlements, making it the cornerstone of any small business coverage plan.

Imagine a cleaning company in Philadelphia that accidentally damages a client's hardwood floors during a routine job. Without general liability coverage, the business owner would have to pay out-of-pocket for repairs and any legal fees if the client decides to file a claim.

Property Insurance & Business Owner's Policy (BOP) in PA

Who it's for: Businesses that own or rent a physical space, or rely on tools, inventory, and equipment to operate.

A Business Owner's Policy (BOP) bundles three essential coverages into one affordable package: general liability, commercial property, and business income insurance. That third component, business income insurance, is often overlooked but critically important. It replaces lost revenue if a covered event forces your business to temporarily shut down.

Consider a retail boutique in Exton, PA that experiences storm damage and has to close for two weeks. A BOP could help pay for building repairs, replace damaged inventory, and cover the income lost while the doors are closed. Bundling your BOP with workers' compensation coverage may also qualify your business for additional premium savings.

Workers' Compensation Insurance in Pennsylvania

Who it's for: Any business with one or more full- or part-time employees.

Pennsylvania law requires most employers to carry workers' compensation insurance. It covers medical expenses and lost wages when an employee is injured or becomes ill on the job. According to the U.S. Bureau of Labor Statistics, private industry employers in Pennsylvania reported 117,400 nonfatal workplace injuries and illnesses in 2024, well above the national average rate, a clear reminder of how quickly things can go wrong for any business, regardless of size or industry.

To understand what that means financially: under Pennsylvania's 2026 Statewide Average Weekly Wage (SAWW), set by the PA Department of Labor & Industry, a single injured employee can qualify for wage-loss benefits of up to $1,394 per week, a 3.5% increase from 2025. That figure alone, before any medical costs are factored in, illustrates why carrying adequate workers' compensation coverage isn't just a legal requirement; it's a financial safeguard every Pennsylvania employer needs.

Imagine a landscaping company in Drexel Hill where an employee injures their back while lifting heavy equipment. Workers' compensation insurance would cover the worker's medical treatment and lost wages during recovery, while also protecting the business from a potentially costly negligence lawsuit.

Cyber & Professional Liability for PA Small Businesses

Who it's for: Service-based businesses, and any company that stores customer data, operates a website, or provides professional advice.

Professional liability insurance, also known as errors & omissions (E&O), protects you if a client claims your work caused them financial harm, even if you believe you acted correctly. Cyber liability insurance covers the costs of data breaches, ransomware attacks, and recovery efforts, an increasingly common threat for small businesses of all sizes.

Consider a bookkeeping firm in Lancaster that makes an error in a client's quarterly tax filing, resulting in unexpected penalties. Without professional liability coverage, the firm would be personally responsible for the legal costs and any damages awarded. E&O insurance bridges that gap directly.

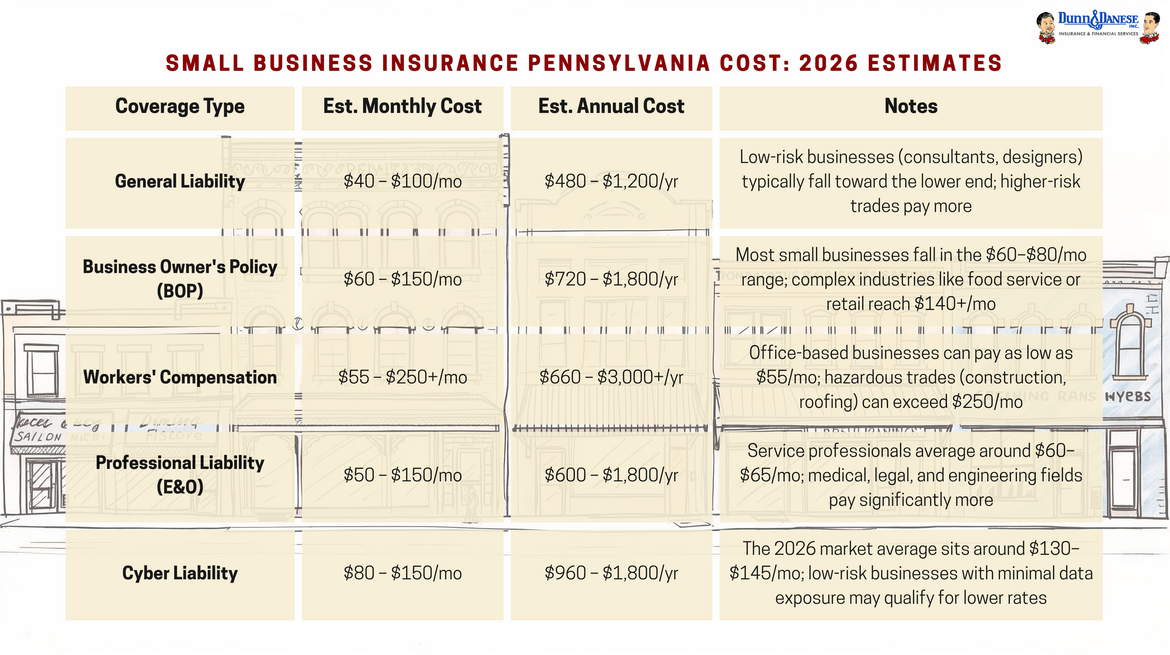

Small Business Insurance Pennsylvania Cost: 2026 Estimates

How much does business insurance cost in Pennsylvania?

There's no universal number; pricing depends on your profession, number of employees, coverage selections, and location.

Your industry has the single biggest impact on your premium. Think about two small businesses: a general contractor in Scranton who operates heavy equipment on active job sites every day, and a freelance graphic designer in Harrisburg who works from a home office. The contractor faces dramatically higher physical risk, and their premium reflects that. Risk exposure drives cost, and understanding that logic helps you budget accurately.

Here are the 2026 market estimates for common Pennsylvania small business coverage:

Estimates reflect 2026 market averages for small businesses in Pennsylvania. Your actual premium will vary based on your industry, payroll, coverage selections, claims history, and location within PA.

These ranges are a starting point, not a final price. The most accurate way to know what your business will pay is to have an independent agent compare live quotes across multiple carriers on your behalf. That's exactly what the team at Dunn and Danese does for every client, at no extra cost to you.

Pennsylvania Small Business Insurance Requirements

Is business insurance required in Pennsylvania?

Yes, in part. Here is what state law mandates:

Workers' Compensation: Required for nearly all businesses with one or more employees. Executive officers and certain domestic workers may be exempt; always verify your situation directly with the state.

Commercial Auto Insurance: Required if your business owns or uses vehicles for work purposes.

Unemployment Insurance: Required for most employers under state and federal law.

General liability and a BOP are not legally required, but most landlords, lenders, and commercial clients will ask for proof of coverage before entering into any contract with you. In practice, they function as business necessities for any professional operation in PA.

How to Choose the Right Small Business Insurance in Pennsylvania

Start by honestly mapping the risks specific to your business:

Do you have employees? Workers' compensation is almost certainly required by PA law.

Do customers or clients visit your location? General liability is essential.

Do you provide professional advice or specialized services? E&O coverage protects you.

Do you store sensitive client or financial data, or operate online? Cyber liability is a smart investment.

Do you use vehicles for deliveries, job site travel, or client visits? Commercial auto insurance fills the gap your personal policy won't.

Once you've identified your exposures, comparing policies and premiums across multiple insurers ensures you're not overpaying or underprotected. That's where an independent agent becomes invaluable.

Small Business Insurance for Startups in Pennsylvania

Many Pennsylvania founders deprioritize insurance in the early stages, a costly mistake that can derail a promising business before it gains traction. Startups typically operate with thin reserves and face accelerating, fast-changing risks as they grow.

At a minimum, a Pennsylvania startup should secure general liability, professional liability if offering any services, and a BOP for bundled, comprehensive protection at an affordable price.

If your startup is structured as an LLC, it's especially important to understand what that protection does and doesn't cover. An LLC (Limited Liability Company) shields your personal assets, your home, savings, and car from business debts. But it does not protect your business from injury claims on your premises, professional errors, cyberattacks, or physical property damage. Insurance fills those gaps directly, and LLC status does not remove the need for proper coverage.

Getting insured early also builds credibility. Investors, enterprise clients, and commercial landlords all routinely ask for a certificate of insurance before moving forward. Having coverage in place signals that your startup is operating professionally and responsibly.

Small Business Insurance in Drexel Hill & Exton, PA

If your business is based in Drexel Hill, Exton, or the broader Delaware County and Chester County region, your coverage needs are shaped by local factors including suburban Philadelphia's competitive market, regional weather patterns, Pennsylvania-specific regulations, and the industries that drive the local economy.

Dunn and Danese proudly serves small businesses across Drexel Hill, Exton, and throughout Pennsylvania with coverage built around your location, industry, and specific risk profile, not generic policies pulled from a national platform.

Why Work With a Local Independent Agency in Pennsylvania

At Dunn and Danese, headquartered in Drexel Hill, PA, with offices in Exton, we are not tied to a single insurance carrier. As an independent agency, we shop across multiple top-rated insurers to find coverage that genuinely fits your business, your budget, and your risk level.

We work with small businesses across a wide range of Pennsylvania industries, including contractors, restaurants, cleaning services, consultants, landscapers, hair salons, manufacturers, and more.

Here's what working with Dunn and Danese means for you:

Multiple carrier quotes, so you're never locked into one option or one price

Local expertise from agents who understand Pennsylvania's business environment firsthand

Ongoing support when you need to file a claim, adjust your coverage, or renew as your business grows

Ready to compare small business insurance options in Pennsylvania?

Get a free quote from Dunn and Danese today.