As a Pennsylvania contractor, you already know you need coverage.

What you need right now is clarity: exactly which policies are legally required, what PA contractor insurance costs in 2026, and where most contractors leave themselves exposed without realizing it.

Here is the complete picture, no generalities.

What Is Contractor Insurance in Pennsylvania?

Contractor insurance in PA is a package of policies, not a single product, built around your trade, crew size, and project types. It simultaneously protects your license, satisfies client and municipal requirements, and prevents one job-site incident from triggering a liability chain your business cannot absorb.

Most Pennsylvania contractors need at least four policies: general liability, workers' compensation, commercial auto, and inland marine. Some trades and project types also require surety bonds and builder's risk coverage. Here is what each covers and what PA law requires.

Key Contractor Insurance Coverages in Pennsylvania

General Liability Insurance for Contractors in PA

General liability is the foundation. It is the first certificate a client, general contractor, or municipality will ask for, and in many cases, it is the first thing standing between your business and a lawsuit.

It covers:

Third-party bodily injury: a visitor or homeowner injured on your job site

Third-party property damage: accidental damage to a client's property during work

Completed operations: claims arising after a job is finished, such as a structure failing months later

Advertising injury: libel, slander, or copyright claims tied to your business

Standard limits for Pennsylvania contractors are $1 million per occurrence and $2 million aggregate. Philadelphia requires a minimum of $500,000 per occurrence for contractors working within city limits. Most commercial projects, lender requirements, and general contractor subcontracts demand limits at or above that threshold.

Workers' Compensation Insurance for PA Contractors

Pennsylvania law requires any contractor with one or more employees to carry workers' compensation. Full-time, part-time, and seasonal workers all count. Sole proprietors are exempt by default but can elect coverage; many clients now require proof of workers' comp regardless of your business structure.

The subcontractor trap is worth knowing: if you bring uninsured subcontractors onto your job site, Pennsylvania law may treat them as your employees, making you liable for their injuries. Always collect current certificates before any sub begins work.

Workers' comp covers medical treatment, wage replacement, and rehabilitation costs for job-related injuries. For trades with real physical exposure, such as roofing, excavation, and framing, skipping it is not a cost-saving move. It is a business-ending risk.

Commercial Auto Insurance for Contractors

Pennsylvania requires commercial auto insurance for every vehicle owned by your contracting business. Personal auto policies exclude business use, and that exclusion will hold under a claim.

Pennsylvania's minimum commercial auto requirements are:

Bodily injury liability: $15,000 per person and $30,000 per accident

Property damage liability: $5,000 per accident

First-party benefits (Pennsylvania's version of personal injury protection): required on all policies

Philadelphia contractors must carry $300,000 in auto liability. Beyond minimums, commercial auto covers physical damage to your own vehicles, hired and non-owned auto liability for employees driving personal vehicles for work, and equipment permanently attached to your truck or van.

For a full breakdown of PA vehicle insurance minimums, see Dunn and Danese's guide to PA Car Insurance Requirements 2026.

Inland Marine Insurance for Tools and Equipment

Standard commercial property insurance covers equipment at a fixed address. Once your tools leave the yard, that coverage typically ends. Inland marine insurance for contractors in PA, also called tools and equipment coverage, protects gear wherever it is: on site, in transit, or stored overnight in a trailer.

It covers theft, accidental damage during use, and loss during transport. In Delaware County and the Philadelphia suburbs, job-site theft is a significant and growing problem. A single break-in can result in $10,000 to $50,000 in equipment losses, and most general liability policies will not cover them.

Surety Bonds for PA Contractors

Many Pennsylvania counties, municipalities, and commercial clients require contractors to be bonded before work begins. A surety bond is not insurance; it is a financial guarantee that you will complete the job in accordance with the contract terms and comply with applicable codes.

Common types include bid bonds, performance bonds, and payment bonds. Under Pennsylvania's HICPA registration requirements, some contractors must also maintain a surety arrangement as part of their registration. Being bonded alongside your insurance coverage signals reliability to clients and opens access to public and municipal contracts.

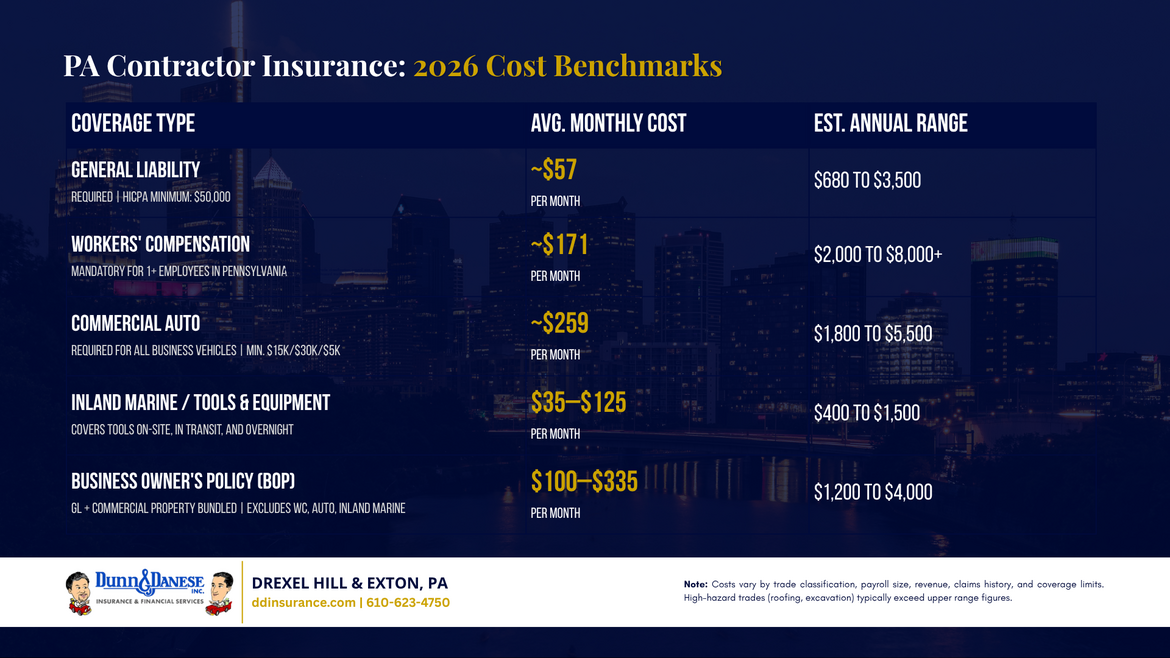

How Much Does Contractor Insurance Cost in Pennsylvania in 2026?

How much is contractor insurance in PA? Based on 2026 market rates across Pennsylvania carriers, here are the 2026 cost benchmarks:

The biggest cost driver is trade classification. A painting contractor pays significantly less than a roofing contractor for identical limits. Other key factors include payroll size, annual revenue, claims history, number of vehicles, and whether you work on residential or commercial properties.

A well-rounded package for a small PA contractor with one or two employees typically runs $3,000 to $8,000 per year combined. High-hazard trades regularly exceed that figure. The fastest way to find the right price is to compare quotes across multiple carriers, which is exactly what Dunn and Danese does for contractors across Pennsylvania.

PA Contractor Insurance Requirements and Licensing

What insurance do you need for a contractor license in PA?

Pennsylvania's Home Improvement Consumer Protection Act (HICPA) requires any contractor performing $5,000 or more in annual home improvement work to register with the Attorney General's Office and carry:

Minimum $50,000 in personal injury liability coverage

Minimum $50,000 in property damage coverage

Those state minimums are a legal floor, not a practical coverage level. Most client contracts, lender requirements, and local permits require substantially higher limits. Philadelphia's per-occurrence GL minimum alone is ten times the state baseline.

PA minimum required insurance coverages vary by municipality and project type. Before submitting any license application, permit, or bid, verify the current requirements with your local licensing authority. Submitting expired or insufficient certificates is the most common reason contractor applications stall or get rejected.

Note: Pennsylvania does not require a statewide contractor business license, but counties, cities, and municipalities each have their own registration and licensing requirements. Electricians and plumbers typically need a specialized trade license in addition to HICPA registration.

General Liability vs. Business Owner's Policy for Contractors

A Business Owner's Policy (BOP) bundles general liability and commercial property insurance into one package, often at a lower combined premium than buying each separately. It makes sense if you own or lease office or storage space and want to consolidate your coverage.

The limitation: BOPs exclude workers' compensation, commercial auto, inland marine, and surety bonds. For most field-based Pennsylvania contractors, a standalone general liability policy offers more flexibility to set limits, add endorsements, and layer in additional coverages as project requirements change. A BOP is a useful starting point, not a complete solution for an active trade contractor.

Contractor Insurance for Small Contractors in Pennsylvania

Small contractor insurance in PA means building the right coverage stack for your actual risk, not defaulting to the minimum required to get licensed.

If you are a solo operator or running a crew of two to three people, your practical baseline looks like this:

General liability: required by virtually every client contract and PA licensing registration

Commercial auto: mandatory for any business-owned vehicle; essential if you are hauling equipment

Inland marine: protects the tools your income depends on

Workers' comp: legally required the moment you hire anyone, even part-time

Surety bond: required for municipal work and many commercial general contractor relationships

Independent contractors who work under a general contractor's direction often assume that the GC's policy covers them. It does not, not for their own tools, vehicles, or liability arising from their own work. Independent contractor insurance in PA is a separate policy requirement regardless of how your work arrangement is structured.

The most expensive gap for small contractors is not having a required policy. It is carrying a policy with no completed operations coverage, no umbrella layer, and no equipment breakdown protection. Those gaps only become visible during a claim.

Contractor Insurance in Drexel Hill and Exton, PA

Contractors working across Drexel Hill, Exton, and the broader Delaware County and Chester County market operate in a compliance-driven environment. Local general contractors, property managers, and municipalities across the Philadelphia suburbs routinely require:

Current certificates of insurance on file before any work begins

Liability limits tied to contract value, often $1 million or above

Additional insured endorsements with specific language requirements

Workers' comp certificates for every subcontractor brought on-site

These requirements change, and they are enforced. At Dunn and Danese, we work with contractors across these communities every day. We know which local general contractors have updated their certificate of insurance requirements, which municipalities have raised their liability minimums, and how to structure your coverage so that paperwork never delays a job start.

Why Choose a Local Independent Agency for PA Contractor Insurance?

A national comparison platform can generate a quote in minutes. A local independent agency can build coverage that actually holds when a claim happens.

At Dunn and Danese, based in Drexel Hill with a second office in Exton, we are not tied to a single carrier. We access multiple admitted and specialty markets and match your trade, payroll, vehicle fleet, and subcontractor situation to the carriers who understand Pennsylvania contractor risk. That is the market we work in every day.

Whether you are a solo residential contractor in Exton, a mid-size general contractor across Delaware County, or a specialty trade professional navigating Philadelphia's permit requirements, we compare your options side by side and make sure you are covered before your next job starts.

Ready to compare your contractor insurance options for 2026?

Get a free quote from Dunn and Danese or call us directly at 610-623-4750.